EUDR - Reading time: 8 Min

The requirements and adherence to EUDR compliance are currently occupying numerous companies from a wide range of industries. Those that work with complex product groups and mixtures of raw materials are particularly affected. Composite products in particular are at the top of the agenda, as it is often unclear at first glance which testing obligations actually apply and how deeply the supply chain must be traced and tested in accordance with the EU Deforestation Regulation. The combination of different materials and raw materials in a single end product in particular often causes uncertainty. The global, multi-layered supply chain also presents companies with new challenges. This article provides a classification for companies, product managers, purchasers and compliance officers.

Because they combine several raw materials with different EUDR references - some in main quantities, some in small proportions - and thus trigger complex supply chains and differentiated inspection obligations that cannot be answered in a generalized manner.

Small parts are therefore also relevant if the end product falls under a listed CN heading.

By checking whether the product is covered by a relevant CN code listed in Annex I, a product falls under the EUDR if it contains / was produced with / (in the case of cattle) was fed with a relevant raw material - regardless of whether the raw material is still 'visible' in the final product."

The CN determines whether a product is fundamentally affected. Only listed CN headings trigger EUDR obligations - supplemented by the TARIC database and specific additions such as "ex", which specifically affect individual subgroups.

As the CN is adjusted annually (e.g. update on 01.01.2026), companies should regularly check CN classifications and affected product ranges against the current CN/TARIC.

Even small quantities of an EUDR raw material - e.g. cocoa powder in a chocolate bar or palm oil in a layer of packaging - may be subject to declaration if the raw material is still identifiable and the CN heading is affected.

In practice, EUDR obligations do not apply if the end product does not fall under a relevant CN heading (Annex I) or if an exception applies (e.g. production before 29.06.2023)."

A structured, interdisciplinary inspection process with clear responsibilities (e.g. purchasing, product management, customs, compliance), technical precision in product descriptions and regular reviews of product ranges and supply chains.

The EU Deforestation Regulation (EUDR) poses considerable challenges for companies, particularly when it comes to composite products. Such products consist of several materials andoften combine different EUDR-relevant raw materials such as wood, cocoa or palm oil, which results in complex supply chains and differentiated testing requirements. The decisive factor for compliance is not just the raw material content, but whether the end product falls under a CN heading listed in Annex I (incl. 'ex' classification) and is therefore considered a relevant product. The Combined Nomenclature (CN) serves as the central classification system here, while 'ex' headings only cover a sub-area of a CN heading and therefore require delimitation via a goods description and, if applicable, TARIC.

To ensure legally compliant classification, companies must establish systematic review processes - starting with the identification of all relevant raw material components, through correct tariff classification to the final assessment of EUDR relevance. Operationally, the processes should also be set up in such a way that the required due diligence declarations (DDS) can be created consistently in the EU information system and referenced internally. Close cooperation between purchasing, product management, customs and compliance is essential. Frequent errors - such as blanket assumptions, inaccurate material descriptions or overlooking hidden raw material components - can be avoided through structured processes, precise documentation and regular portfolio analyses. The article thus provides a practical guideto effectively implementing regulatory requirements and minimizing risks in relation to EUDR violations.

More and more everyday and capital goods consist of numerous individual components sourced from very different raw materials. However, the EU Deforestation Regulation targets specific groups of raw materials, above all wood, cocoa, coffee, soy, palm oil, cattle and rubber, as well as individual products made from these. Composite products break through this categorization, as they combine several of these raw materials - sometimes as the main ingredient, sometimes in traceable small quantities or as a component of intermediate products. This inevitably leads to a number of special testing requirements for which a suitable solution must be found in order to efficiently meet regulatory requirements.

A great deal of uncertainty arises primarily due to material mixtures and the complex international supply chain. Many companies are faced with the task of carrying out a reliable and legally secure assessment for products with a proportion of EUDR-relevant raw materials (such as furniture with wooden frames, packaging coated with palm oil, chocolate bars with cocoa powder) - including the requirement to provide geolocalized proof of the parcels of origin of all relevant raw materials contained in relevant composite products. Products whose raw materials have contributed to deforestation and deforestation may not be placed on the EU market or exported from the EU if the requirements are not met. Companies must prove that the raw materials are deforestation-free (cut-off date 31.12.2020) and have been legally produced in accordance with the law of the country of production.

In addition, due diligence declarations (DDS), risk analysis and, if applicable, supporting evidence (e.g. audit reports, standards, certificates as information modules) must be available for the above-mentioned processed raw materials in order to guarantee freedom from deforestation. The audit intensity can also vary depending on the country risk classification. At the same time, unclear responsibilities within the organization and a lack of transparency in partial supply chains pose additional risks for compliance and EUDR conformity.

The term "composite products" refers to end products that combine several individual materials. The term 'composite products' is a practical term; the EUDR refers to relevant products that contain or are manufactured with relevant raw materials or products. These composite articles consist of different raw materials that are processed in varying proportions to form a new product. Typically, this combination results in a product with different properties than the sum of its individual parts. A precise demarcation is essential in the EUDR and customs context: simple homogeneous products such as pure wooden boards or cocoa powder can be clearly demarcated. However, if a cabinet consists of wood, metal and glass, or if packaging contains a laminated layer of palm oil, it is referred to as a composite product.

The example of furniture illustrates the complexity particularly well. A piece of seating furniture often consists of a steel structure, wooden panels, plastic upholstery and textile covering. Whether the piece of furniture itself is an EUDR-relevant product is determined by the CN classification according to Annex I (including 'ex' classifications). If the piece of furniture is relevant, the relevant raw materials that it contains or with which it was manufactured must be fully covered, including geolocation of all parcels of origin.

The issue is even clearer in practice with beverage cartons: here, paper (made from wood), plastic (usually from crude oil) and aluminum are processed into a composite that can hardly be separated from one another in terms of quantity. Rubber products with a proportion of natural rubber and synthetic components also give rise to a differentiated examination, as only natural rubber (Hevea brasiliensis; usually CN/HS 4001 or, in the case of derived products, partly 'ex') is covered by EUDR. Important: Packaging is only EUDR-relevant if it is placed on the market as an independent product. Pure transport or protective packaging of another product is generally no longer covered.

In the food industry, the challenge is seen in chocolate products, for example, in which cocoa powder, cocoa butter, milk powder and various fractions of palm oil are processed together. Although the cocoa content of a chocolate bar usually only accounts for a fraction of the total mass, the raw material origin of the cocoa it contains plays a key role for the EUDR. These so-called composite products often have complex supply chains. Depending on which raw materials are included, different obligations may apply under the EUDR. The prerequisite is that the end product falls under a relevant CN heading (Annex I). In this case, the origin or geolocation of the relevant raw materials used must be documented, even for highly processed formulations.

The EUDR is linked to selected raw materials and the products listed in Annex I. The decisive factor here is not "materiality" or a certain minimum proportion, but the legal classification via the customs tariff number (CN) and the goods description in Annex I. If an end product (including composite products) falls under a listed CN heading, the EUDR obligations apply; the relevant raw materials/products that the product contains or with which it was manufactured must then be mapped for the quantities concerned in the DDS, risk analysis and certificates (deforestation-free and legal).

Whether a product is subject to EUDR compliance is primarily determined by looking at Annex I of the regulation. This Annex lists all the raw materials and associated products concerned on the basis of the Combined Nomenclature (CN headings). Please note: Only products that fall under a listed CN heading are affected at all and are required to provide information. This limits the obligation to check and prevents all complex goods from having to be checked across the board. In the case of items marked "ex", it is also necessary to check which part of the CN heading is actually covered, often via TARIC or subdivisions.

For companies that trade in or import composite articles, there are three key criteria for assessing relevance in practice.

A classic example of practical classification is the export or import of finished furniture with a visible or invisible wood component, such as a veneered shelf. As furniture with wood content is shown in detail in the CN, the reference to the EUDR can often be clearly established - provided that the piece of furniture falls under a commodity code listed in Annex I. In this case, all original parcels of the relevant wood components must be geolocalized for composite wood elements.

In the confectionery sector, the decisive factor is whether the end product falls under a CN heading listed in Annex I. There is no general minimum quantity. The abbreviation "ex" indicates that only a part of the respective CN heading is covered.

A distinction must be made for packaging: If the packaging is placed on the market as an independent product, it may - depending on the CN/Annex I listing - be EUDR-relevant. If it is used exclusively to support, protect or carry another product, it is generally not covered by EUDR. In practice, such classification and delimitation issues are often clarified with customs, specialist departments and, where applicable, the competent authorities.

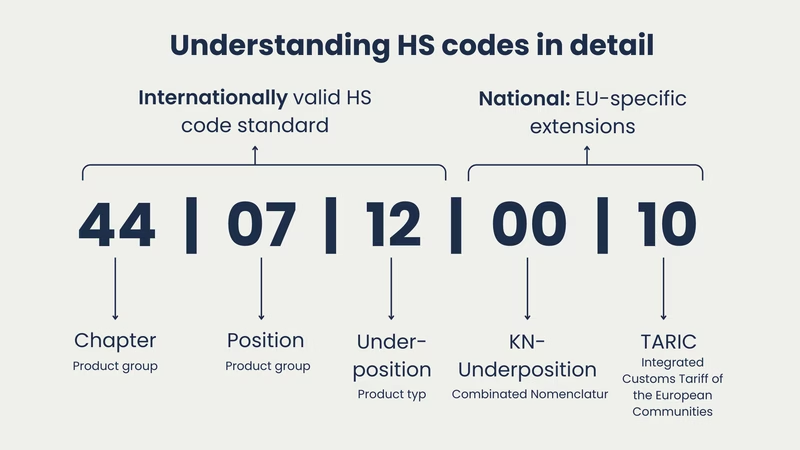

The Combined Nomenclature (CN) is the central system for classifying goods in the EU customs tariff. Based on the globally valid "Harmonized System" (HS), the CN offers a finer subdivision tailored to EU requirements and codes goods according to eight-digit codes. The CN is updated annually (e.g. valid version from January 1, 2026), so CN classifications should be checked regularly against the current version. These are used both for customs classification and as a reference for numerous foreign trade regulations and are at the heart of the EUDR relevance check. For operational delimitation (e.g. for 'ex' items), TARIC is often also used, which supplements the CN with further EU subdivisions.

Although the HS classification forms the first basis for tariff classification, it is international and therefore often offers a less granular distinction than the EU CN. The latter goes deeper with additional numerical levels and is decisive for tariff classification in the EU customs tariff. This additional level of detail is particularly important in the context of the EUDR: many products consisting of mixtures of raw materials can only be clearly assigned to the regulation based on their CN number.

The term "ex" in Annex I of the EUDR indicates that only part of a CN heading is affected - for example, only products made of wood, but not those made of other materials. This can mean that not the entire CN heading is covered, but only the subheading described in the Annex. Depending on the case, the distinction is made via the goods description and, if necessary, via TARIC subdivisions. At this point, companies must not classify the entire CN heading as EUDR-relevant, but must check exactly which subcategories are affected and how these are mapped in their own product range.

In practice, it is therefore essential to look at the details. The EU's TARIC database expands the Combined Nomenclature to include national characteristics and specific foreign trade regulations - these can also be relevant for EUDR compliance.

The TARIC database is the EU's integrated customs tariff and links the CN with EU-wide measures from customs, trade and agricultural law in order to enable uniform application in all member states. In practice, the applicable CN heading is determined via TARIC - supplemented by tariff explanations/annotations and, if necessary, binding tariff information (BTI) in the event of uncertainty. As the CN is updated annually, CN mappings should be checked regularly against the current version.

It is crucial that the product description is stored clearly and technically correctly in the company's own systems. This forms the basis for legally compliant tariff classification and subsequent documentation. As part of EUDR compliance, it must also be ensured that all relevant product groups are continuously reviewed, especially if supplier structures, material compositions or product portfolios change. The technical documentation should therefore not only accurately reflect the final product, but also the raw material fractions it contains.

The necessary check as to whether a composite product is subject to the EUDR is carried out in several steps. The first step is to identify the product and all relevant raw material components along the supply chain. The second step is the tariff classification based on the CN and TARIC data. This is followed by a comparison with the listed items in Annex I of the EUDR. Once the end product has been recorded, the EUDR obligations (including geolocalization/legality/risk analysis) apply and a due diligence declaration (DDS) must be filed in the EU information system before the product is placed on the market or exported. However, this serves as preparation, as the obligation to perform further due diligence, in particular documentation, reporting and traceability obligations, only arises once all these verification steps have been completed.

Practical tools and checklists can efficiently support this process. Companies that regularly work with material mixtures should create a database for the standardized classification of their product ranges and integrate automated reconciliation processes with CN and TARIC codes. In addition, companies should align their processes with the EU information system (DDS register) (roles/workflows, reference numbers, interfaces). The amendments of December 2024 and December 2025 also introduced simplifications that can reduce the administrative burden for certain downstream actors in particular - the data and cooperation obligations in the supply chain nevertheless remain central.

Especially in the case of composite products, an isolated approach by individual departments is rarely effective. Instead, interdisciplinary cooperation should be established. Purchasing provides information on the primary product and suppliers, while product management knows the composition and can document changes. The customs department is an expert in correct tariff classification and can identify risks within the framework of the EUDR. Finally, the legal or compliance department checks compliance with due diligence obligations and provides information on appropriate documentation and communication with authorities. It is best to set up an internal review process in which responsibilities and review deadlines are clearly defined - for example, through an internal compliance board or a regular coordination meeting for new products or changes to the product range.

A common mistake in practice is the basic assumption that every raw material component in a product makes the entire end product EUDR-relevant. In reality, however, the CN heading and Annex I comparison must always be considered together before a notification obligation is assumed. Blanket assessments, for example on the basis of parts lists or rough material descriptions, should therefore be avoided. The relevance of "hidden" raw material components is also often underestimated: In many cases, EUDR raw materials are only indirectly present, for example as an adhesive component, coating or in auxiliary materials.

Special care is required here: The trigger is the Annex I/KN relevance of the end product, not the 'visibility' of individual components. Once the product has been recorded, indirect raw material components, insofar as they fall under the EUDR logic, must also be mapped in the data and verification process.

Checking the EUDR coverage of complex and composite products requires a coordinated, systematic approach - and a reliable classification via the Combined Nomenclature. Annex I of the EUDR defines the scope of application via CN headings (including "ex" classifications), while TARIC and the technical description of goods help in practice to correctly determine the exact subgroup and avoid misclassification. As the CN is updated annually, the internal mapping should be checked regularly against the latest version.

Companies should carry out a structured portfolio analysis at an early stage in order to identify EUDR-relevant product groups, affected raw material flows and critical supply chain sections. Consistent prioritization according to Annex I/KN relevance creates efficient use of resources and reduces the risk of gaps in due diligence. At the same time, a regular reassessment is recommended in the event of changes to the product range, recipe, material or supplier - including updating data points for traceability and geolocalization. Operationally, the process should be set up in such a way that the due diligence declarations (DDS) are consistently stored in the EU information system and can be referenced internally in a traceable manner.

Complete, auditable documentation of all tariff classification decisions, data sources, risk assessments and approvals is not only a compliance requirement, but also an effective protective instrument in the event of inspections and queries by customs and market surveillance authorities. This means that EUDR implementation does not become a reactive, case-by-case process, but a resilient, scalable system for product and supply chain compliance.

The EUDR obligation only applies if the product falls under one of the CN headings listed in Annex I, which relates to one of the seven relevant raw materials. For composite products, the CN classification according to Annex I (incl. 'ex' delimitation) is decisive. Whether the raw material is mentioned in the description text can be an indication, but is not mandatory.

The HS code provides the basic international classification of goods, while the CN codes are the EU-specific classification system based on this, with a greater level of detail. Classification according to CN/Annex I is decisive for the EUDR. In practice, TARIC is often also used for clarification (especially for 'ex' items).

Companies must check at least the position of the listed CN number and the specific product specification. In case of uncertainty, it is advisable to consult with the customs authority or obtain binding tariff information. It is important to document the classification decision and the underlying product description in such a way that it can be consistently verified later for DDS/authority audits.

Particularly in complex supply chains with multiple production steps, manufacturing stages and material mixtures, it is crucial to obtain comprehensive information from the entire chain. Anyone acting as an importer remains responsible for the complete documentation of all relevant raw material components. Any market participant who places a relevant product on the EU market for the first time or exports it remains responsible for the full due diligence declaration and the underlying information - even if data originates from sub-suppliers.